Top earners respond to changes in income taxation

A recent study by Reetta Varjonen-Ollus examines how raising the top marginal income tax rate affects the incomes of high earners.

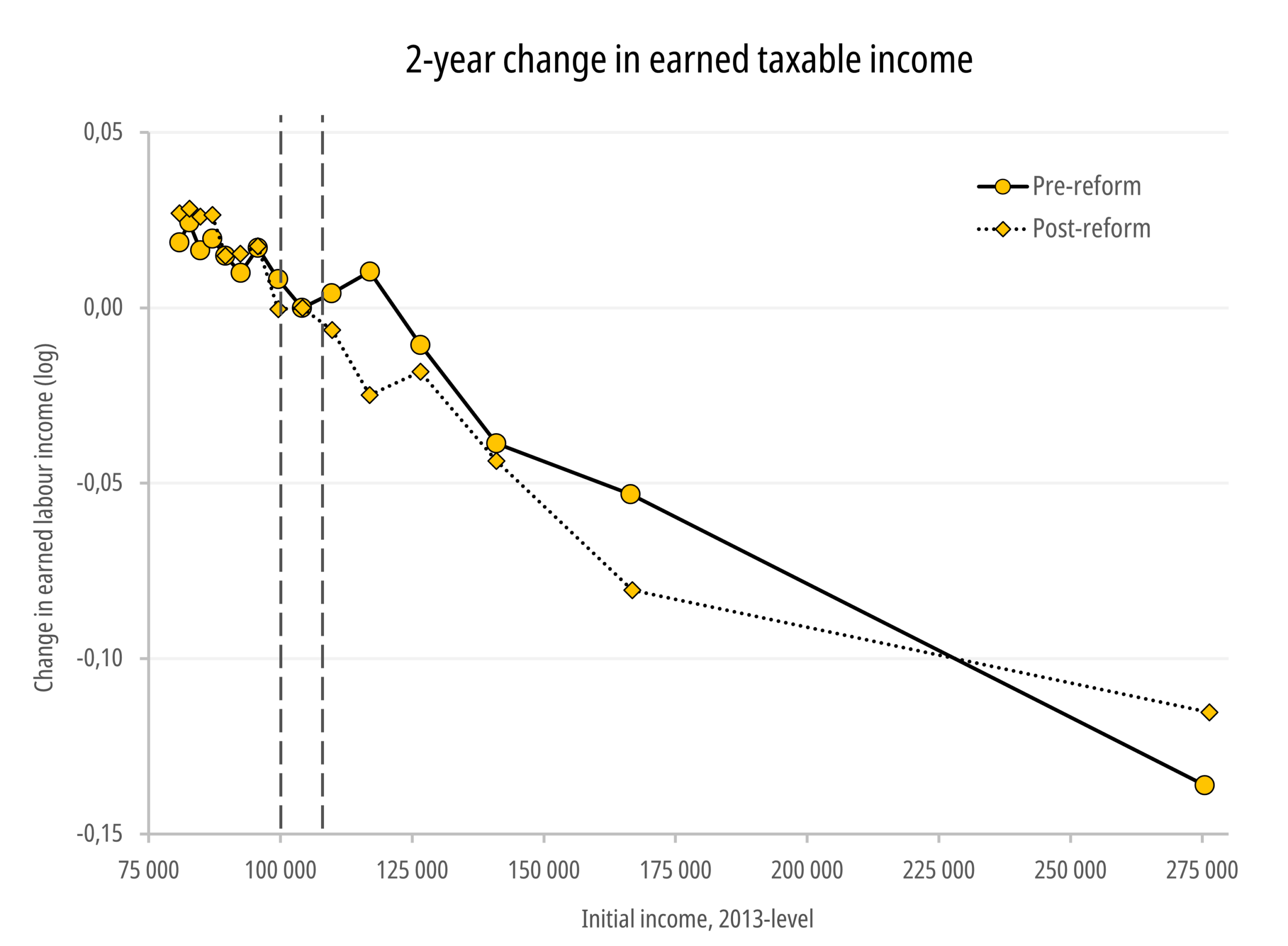

Doctoral researcher Reetta Varjonen-Ollus (University of Helsinki, FIT) studied how raising the top marginal income tax rate affected the incomes of high earners. The study used as a natural experiment the “solidarity tax” introduced in 2013, which increased the top income tax rate by two percentage points for individuals earning more than €100,000 per year in wage income. The reform affected the top one percent of income earners, concerning about 40,000 people.

The study finds that the taxable income of individuals subject to the solidarity tax decreased after the marginal tax rate increase compared with the control group. The effect of the increase in the top tax rate is observed both in earned income and in total income, which includes capital income in addition to earned income. According to the results, the elasticity of taxable earned income among the highest-earning wage earners is 0.5, and for total income it is 0.4.

The study also examined the tightening of marginal taxation in 2016, which affected individuals earning approximately €79,000 – €90,000 per year. For this group, no corresponding clear behavioural effects were observed.

The study provides new evidence on behavioural responses, particularly using Finnish data, and its findings can be used in ex ante evaluations of economic policy. Based on the results, lowering the top marginal tax rate would increase the taxable income of high earners, meaning that tax cuts targeted at them could largely finance themselves. This finding is consistent with other recent studies conducted in the Nordic countries.

The full text of FIT Working Paper 39:

Reetta Varjonen-Ollus (2025) Behavioral Effects of a Top Marginal Income Tax Rate Increase. FIT Working Paper 39/2025.